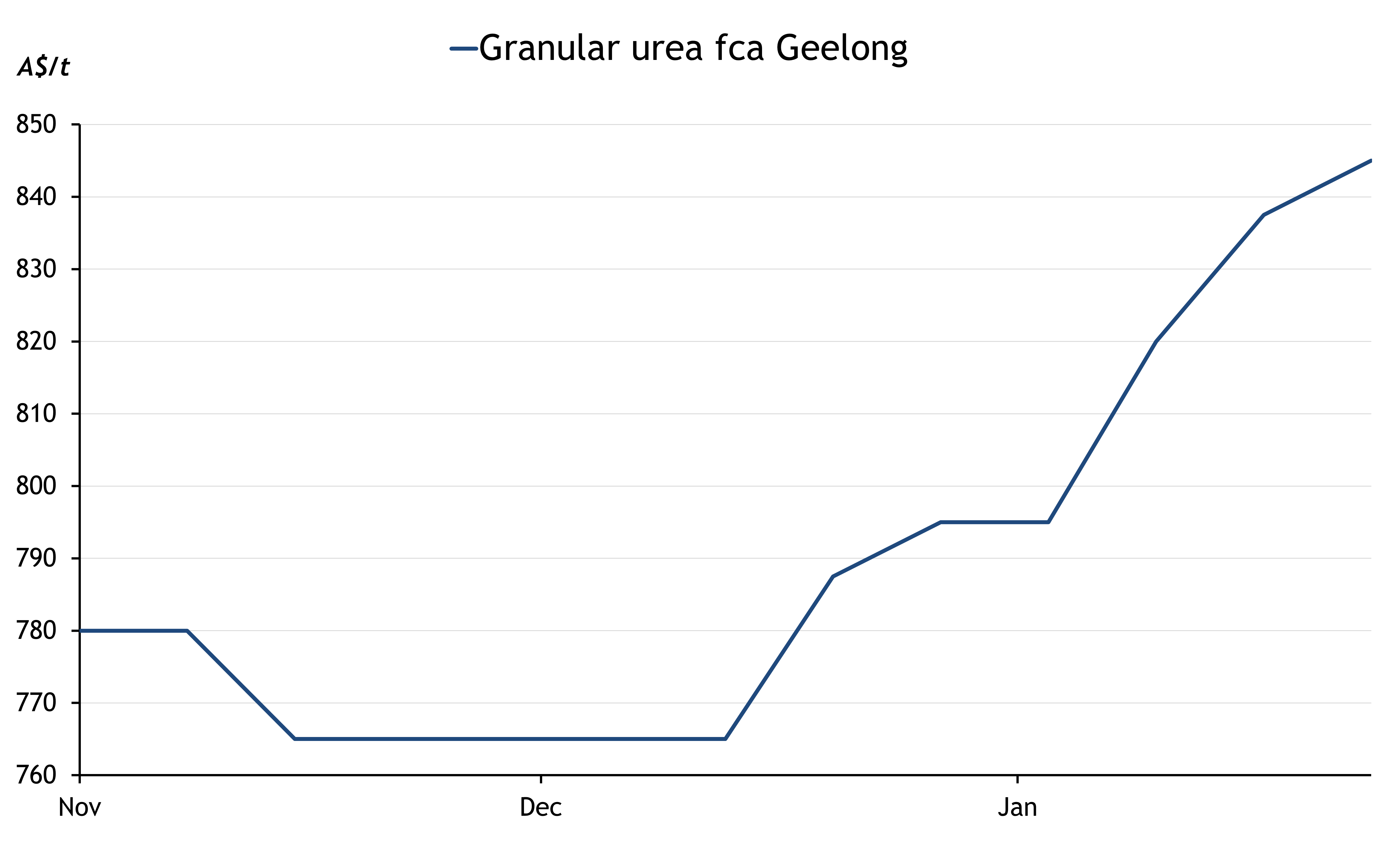

Urea

Domestic demand for granular urea was slow while the market watched and waited to see the impacts of India’s latest tender.

India was able to secure just over 1.3 million tonnes of urea across its west and east coasts and the lowest offer prices were significantly higher than the country’s previous tender in January.

Argus last assessed granular urea at A$840-850/t fca Geelong, reflecting the current international free on board (FOB) prices that jumped in late January.

There was 1-50mm of rain forecast for all of South Australia and Victoria on 22 February, according to the Australian Bureau of Meteorology. Much of New South Wales and Queensland were also expecting to receive rainfall from 22 February. This rainfall may encourage growers to enter the market for urea purchasing.

Phosphates

Domestic MAP/DAP demand was confined to small parcels, with no major buying occurring.

There are 270,000t of MAP/DAP and other phosphorus fertilisers in transit to Australia, vessel tracking data from Kpler show. These are made up of five vessels from Saudi Arabia and two from Morocco.

Australia needs to consider CBAM impact on agriculture

Australia needs to consider the associated impacts a carbon border adjustment mechanism (CBAM) would have on the cost of critical inputs for the country's agriculture sector, specifically for fertilisers like ammonia and derivatives like urea and ammonium phosphate, key farming group the National Farmers' Federation told Argus on 18 February.

Rail subsidy to benefit Australian phosphate producers

The Queensland government today clarified terms for the four-year rail subsidy it had promised Australian phosphate producers last year.

Under the terms, Australian phosphate producers will be able to save A$2.80/t ($1.98/t) for moving 500,000 t/yr of mineral concentrates from Cloncurry to Townsville port.

Commentary and pricing supplied by Argus Media

Disclaimer: The information provided in this report is general in nature and is intended for informational purposes only.